Ensuring all citizens have access to mobile and fixed networks is a priority for many governments around the world. However, providing connectivity in sparsely populated rural regions of any country is usually commercially challenging. As a result, several governments – including the UK – are looking at Shared Rural Networks (SRN) as a solution to improve coverage in their countries.

Overview of UK SRN

The UK’s SRN project is a joint operator and government initiative designed to improve mobile coverage in the rural areas of the four nations of the UK: England, Northern Ireland, Scotland and Wales. The overall objective of the project is to increase total 4G coverage of the UK landmass to 95% by 2026. The SRN project is essentially divided into two parts as follows:

- Phase 1: 4G Partial Not Spots (PNS) – defined as areas where at least one operator provides 4G coverage, but not all four of them.

- Phase 2: 4G Total Not Spots (TNS) – defined as areas that currently do not receive 4G services from any operator.

The UK’s four operators – EE, O2, Three and Vodafone – are sharing the costs of rolling out the new infrastructure on an approximately 50:50 basis with the government, with the operators contributing to Phase 1 and the government financing Phase 2. Total cost of the project amounts to approximately $1.4 billion (£1.032 billion).

SRN Coverage Obligations

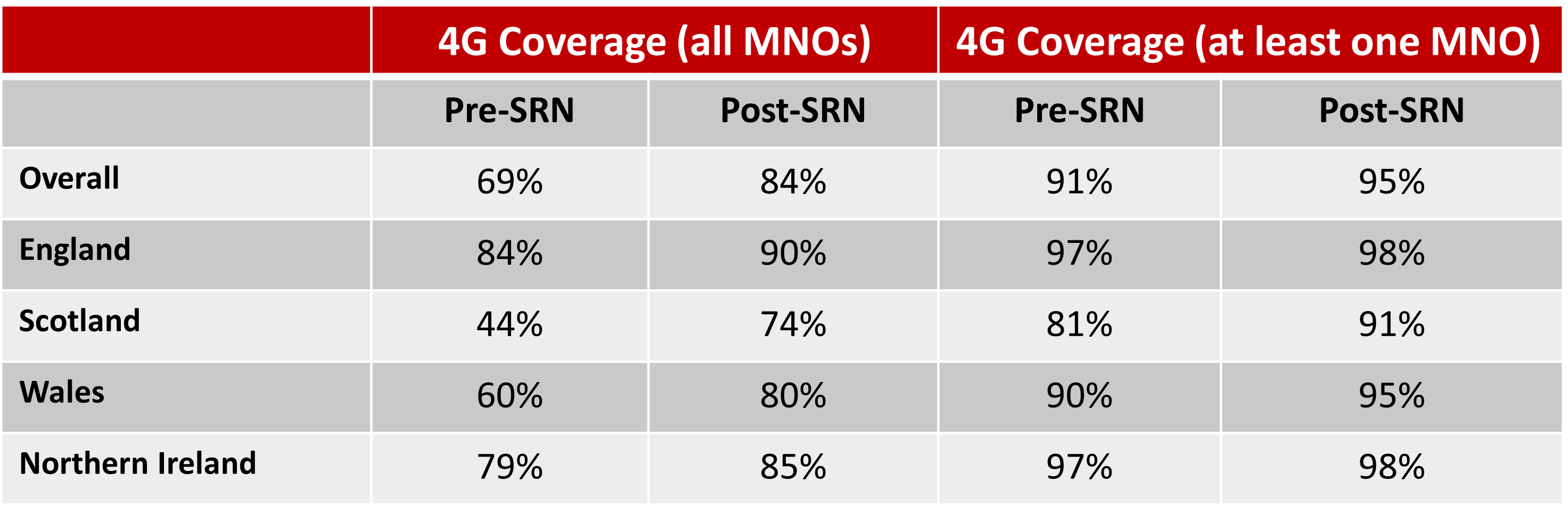

Although individual coverage targets vary from nation to nation, as shown in Exhibit 1, the goal is to raise 4G coverage from all four operators to 84% by the end of 2024 and ensure that 95% of the UK’s landmass is covered by at least one operator by the end of 2026. This should ensure 4G coverage to an additional 280,000 premises, 16,000 km of roads as well as improve indoor coverage in around 1.2 businesses and homes.

Three of the operators – O2, Three and Vodafone – have agreed to build a total of 222 new towers for Phase 1, of which 124 will be in Scotland, 54 in England, 33 in Wales and 11 in Northern Ireland, with each operator leading on 74 of the new sites. Although sharing towers and sites, each operator will procure and operate their own active equipment, i.e. antennas, radios, basebands, etc. However, the exact number and location of masts will depend on the ability to find suitable sites, obtaining power supply, backhaul services and securing the necessary planning permissions.

Image may be NSFW.

Clik here to view. ©Counterpoint Research; Source: Digital Mobile Spectrum Ltd.

©Counterpoint Research; Source: Digital Mobile Spectrum Ltd.

Exhibit 1: SRN Coverage Obligations

EE is contributing to Phase 1 by expanding its existing 4G coverage – primarily through upgrades – to more than 2,000 sites by 2024. Since March 2020, a total 853 sites have been upgraded, including 449 in England, 254 in Scotland, 97 in Wales and 42 in Northern Ireland. A further 1,500 upgrades are expected by 2024.

Emergency Services Network

Separately, the UK government is financing the construction of a new emergency services network (ESN) across the UK. Built and operated by EE, with equipment provided by Motorola Solutions, the ESN will also consist of 292 Extended Area Service (EAS) sites financed by the UK government to ensure coverage in some of the most remote parts of the UK. These EAS towers will be available for other mobile operators to offer commercial services as part of their SRN network committment. Achieving the coverage data shown in Exhibit 1 will depend upon the availability of these EAS sites.

Project Status and Schedule

Operators in Phase 1 are in the process of securing sites, reaching rental and access agreements with site owners and obtaining the necessary permissions from planning authorities. Although a small number of PNS sites have already been deployed, the main build out is expected to start sometime in 2H 2022. Clearly, progress will depend on cooperation with the various rural communities. Counterpoint Research understands that two of the operators are expected to announce their preferred hardware vendors within the next month or so.

In the case of Phase 2, contracts to design and build the towers, install base station hardware and manage the TNS sites have been awarded with the winning bidders being: Clarke Telecom, Killarney Telecommunications, Mitie Technical Facilities Management and WHP Telecoms. In addition, a tender notice to supply the backhaul transmission network for the TNS sites was issued in May 2022.

Viewpoint

The UK’s operators have chosen not to adopt a neutral hosting approach, which involves the sharing of base station equipment. There is also no pooling of spectrum, resulting in less efficient spectrum utilization. In fact, sharing is largely limited to towers and sites. Counterpoint Research suspects that this was the only way to ensure operator agreement and committment to the project. In addition, the network is a mobile-only network and does not provide any provision for fixed broadband access. Other countries such as Finland and New Zealand have adopted combined mobile and broadband network designs, also with active equipment sharing and spectrum pooling.

Although the UK’s SRN project will undoubtedly improve 4G coverage across large swathes of the UK, it will not deliver coverage to all communities. In particular, aggregate 4G coverage in Scotland will only increase to 74% with limited, i.e. one operator, or no coverage at all across almost a quarter of its remaining landmass. In addition, the operators are up against some tight deployment deadlines, with Phase 1 scheduled to be completed by the end of 2024 – less than two and a half years away.

Finally, rural networks – whether shared or otherwise – should be a golden opportunity for open RAN to deliver on its many promises. Although the UK government is championing its use in the UK, there is, however, no obligation on operators to adopt the technology in this project. As a result, Counterpoint Research expects that all four operators will choose tried and tested, proprietary 4G infrastructure from established vendors Ericsson and Nokia – with perhaps an outside chance that Vodafone will plump for open RAN compliant tech from existing supplier Samsung Networks at some of its sites.

Related Blogs And Reports

Open RAN: Again a Hot Topic at MWC

Chip Vendors Showcase Open RAN Merchant Silicon Solutions at MWC

Open RAN Cheerleader Vodafone Plays Safe with Incumbent Vendors

Open RAN Radios – Chinese Vendors Set To Dominate An Emerging Market?

The post UK Operators Face Tight Deadlines to Roll Out Shared Rural Network appeared first on Counterpoint.